GLOBAL ECONOMICS AND POLITICS

Leo Haviland provides clients with original, provocative, cutting-edge fundamental supply/demand and technical research on major financial marketplaces and trends. He also offers independent consulting and risk management advice.

Haviland’s expertise is macro. He focuses on the intertwining of equity, debt, currency, and commodity arenas, including the political players, regulatory approaches, social factors, and rhetoric that affect them. In a changing and dynamic global economy, Haviland’s mission remains constant – to give timely, value-added marketplace insights and foresights.

Leo Haviland has three decades of experience in the Wall Street trading environment. He has worked for Goldman Sachs, Sempra Energy Trading, and other institutions. In his research and sales career in stock, interest rate, foreign exchange, and commodity battlefields, he has dealt with numerous and diverse financial institutions and individuals. Haviland is a graduate of the University of Chicago (Phi Beta Kappa) and the Cornell Law School.

Subscribe to Leo Haviland’s BLOG to receive updates and new marketplace essays.

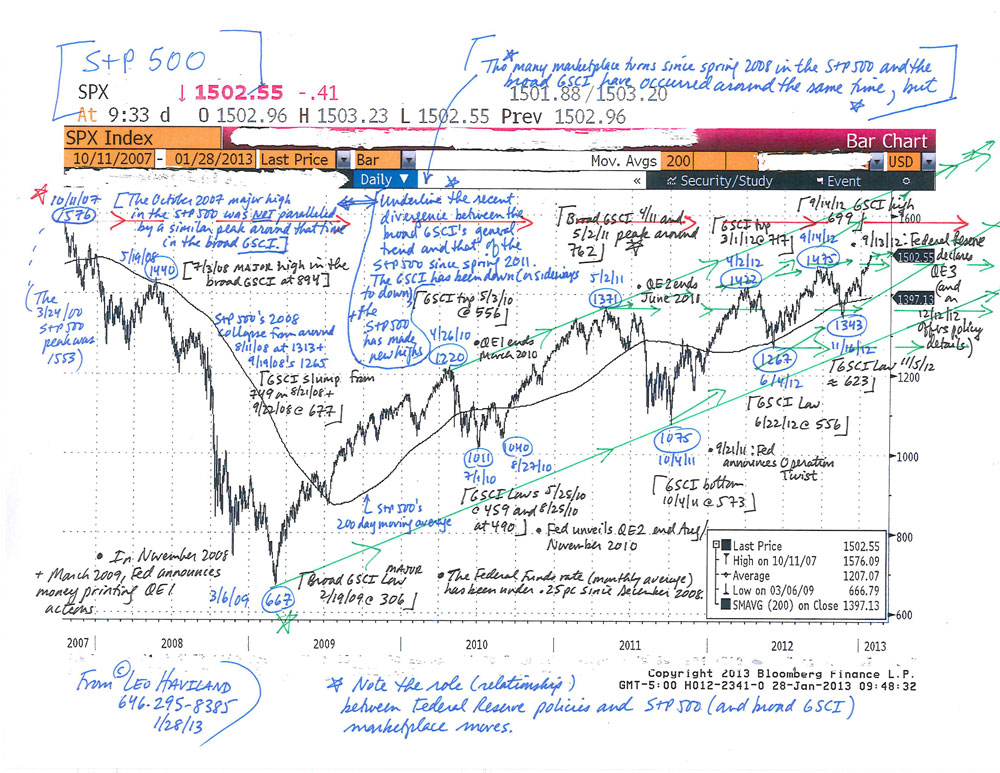

Since mid-2008, commodities “in general” and United States stocks “as a whole” have moved roughly in the same direction at around the same time. In this convergence process (relationship), noteworthy bull (bear) moves in US equities find parallels in those in the commodity arena. Thus significant marketplace rallies (declines) have tended to occur around the same time.

However, this perspective is not the only vantage point by which to assess the often close relationship between US equities and the commodities complex. There also is another, longer run view by which one can examine the relationship between them. Since spring 2011, commodities have ventured down (or sideways to down). However, key American stock benchmarks such as the S+P 500 have attained new highs, first in April 2012, then September 2012, and again in January 2013. Thus despite the convergence at assorted timely turning points since spring/ summer 2008, and even though the two territories continue to trade together to some extent, arguably there has been noteworthy divergence in their overall relationships (their trends) since May 2011.

Now recall several of 2007-08’s details. US equities peaked in October 2007, almost nine months before the commodity one in early summer 2008. Only after the final stock marketplace

summit in May 2008 did equities and commodities trade in close tandem. The current longer run relationship thus perhaps likewise reveals divergence, but with the commodity peak to date appearing well before any major S+P 500 one.

In contrast to 2007-08, what if the major peak in commodities is well before that in stocks (and the lag is likewise so great as to suggest divergence)? Suppose- and this admittedly is a key suppose- eventually commodities and US stocks will trade together over the long run. After all, so-called marketplace relationships can change dramatically, whether from the convergence/ divergence (lead/lag) perspective or otherwise. What does continued divergence, the failure of commodities to near or exceed its spring 2011 heights, suggest?

The 2007-08 relationship warns that the current continued failure of commodities to confirm the equity rally eventually will reveal a notable decline in stocks. Since the duration between the spring 2011 commodities top and today’s new highs in the S+P 500 is almost 20 months, whereas that between October 2007’s stock pinnacle and the broad GSCI’s summit in July 2008 was about nine months, the failure of the broad GSCI to achieve new heights should warn equity bulls that a decline may be fairly near in time.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Commodities and US Stocks- Convergence and Divergence (1-28-13)

S+P 500 Chart (1-28-13, for essay on Commodities and US Stocks)

The world’s long-running economic crisis of course has not limited itself to either one nation or one region. However, at its outset in 2007, most did not anticipate the scope or length of the disaster. Weren’t potential risks to the international economy rather modest? Weren’t issues related to the United States real estate marketplace mostly relevant only to that domain and that nation, and likely to be restricted to them? Yet substantial debt and leverage (and other intertwined issues) and their consequences were not confined either to American territory or the real estate playground.

The recent Eurozone chapters of this terrible trouble supposedly started with so-called peripheral nations such as Greece, Portugal, and Ireland. Countries such as Greece indeed first captured headlines. However, that does not demonstrate that causes of Eurozone problems necessarily started only in them. In any event, “difficulties on the periphery” engulfed the rest of Europe and traveled around the globe.

Despite broad concerns regarding worldwide economic problems and risks, despite the widespread past and current fascination with the European scene, suppose one focuses on aspects of the American stage, beginning with some highlights involving the United States alongside Canada and Mexico in the foreign exchange context. This survey of America and its geographic neighbors underlines the weakness of the United States dollar and the size of America’s fiscal troubles. This suggests the merit of inquiring into US currency, stock, interest rate, and commodity marketplace past and future relationships in the context of Federal Reserve easing policies and America’s fiscal problems.

The broad real trade-weighted dollar probably will continue to weaken. The dangerous United States fiscal situation probably will not be genuinely fixed in the next several months. A full- fledged threat of a federal fiscal catastrophe likely will be necessary for sufficient progress in that sphere to occur. Though the United States is not the center of the universe, the effects of further dollar feebleness and the worsening of the country’s fiscal crisis will radiate worldwide.

The S+P 500 has made or soon will make a significant peak.

Thus the emerging (current) story and trend appears to be: weaker dollar (TWD), weaker S+P 500, and higher government rates (UST 10 year benchmark). This vision admittedly is dramatically different from the current popular faith in these marketplace relationships.

-1")

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

American Marketplaces- At the Crossroads (10-15-12)

Charts- US Dollar v Canadian Dollar, Mexican Peso (10-15-12)

To create a sustained and substantial recovery, gurus and their audiences agree that much matters on the fiscal front. In the darker days of the economic crisis, most financial sentinels and their allies proclaimed that large sustained fiscal deficits were good (or at least acceptable, up to some point). Whatever have been the short term benefits of enthusiastic deficit spending campaigns in America and elsewhere, epic fiscal measures only shifted some of the debt (and leverage) burden from the private sector to the public one.

However, nowadays big sovereign debt generally is viewed as a problem. Most of the public hopes that noteworthy fiscal progress to reduce terrifying deficits has been made, is being achieved, or eventually (and soon enough) will be accomplished.

Let’s spend time surveying some fine print regarding the fiscal landscape, paying particular attention to Europe and America. At best, only limited advances have been made in recent wars against huge deficits. Actually, judging from their very modest results, these struggles to slash them look more like skirmishes than pitched battles.

A Financial Times front page headlines the European Union’s “tough fiscal treaty” (1/31/12; this refers to the “Treaty on Stability, Coordination and Governance in the Economic and Monetary Union”). Many applaud this treaty for its alleged fiscal hard line. It indeed takes a step towards resolving Europe’s sovereign debt and banking crisis, but a small step is not a giant leap. Despite the stagecraft of European leaders, the region’s fiscal challenges are not near to being resolved.

Though many states and municipalities face scary times, let’s focus on the federal deficit. The US fiscal situation remains fearful.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Fiscal Fine Print (2-7-12)

Recent historically high nominal United States corporate profit levels are a key factor inspiring many to buy and hold US stocks. Bullish forecasts regarding future net earnings, especially when such predictions extend out to misty medium term or murky long run time horizons, sustain and bolster this enthusiastic ownership. In turn, stock rallies sometimes boost optimism regarding potential corporate profitability and overall economic growth, for many have faith that equity marketplaces are forward-looking indicators for “The Economy”.

Has the US entered a blessed New Era of very high corporate profitability that will stretch happily out into the indefinite future? Probably not. Has America revived the wonderful time of the Goldilocks economy? Probably not. Higher nominal corporate profits and ascending nominal stock prices, when accompanied by rising nominal GDP, can assist national confidence and encourage spending in the short term. However, since the nominal levels are not the real (genuine) ones, they do not translate into an equivalent amount of real and permanent prosperity.

Yet even if very elevated corporate profitability does not continue, what may have caused a sustained notable upward shift relative to long run history in the ratio of nominal US corporate profits to nominal GDP? To some extent, it reflects corporate cost-cutting measures and other battles to improve efficiency. The easy money policies of the Federal Reserve Board (sustained low interest rates; money printing) and its allies and massive deficit spending (stimulus) perhaps play roles. But picture the context of sluggish to declining real US household income, still-damaged consumer balance sheets, high unemployment, weak housing prices, and very low consumer confidence. With that domestic (home) background, high US nominal corporate profits- and especially a more elevated nominal profit versus GDP ratio- also arguably reflects economic globalization trends and profits captured from overseas. If so, then relatively high American corporate profits do not entirely reflect (do not fully represent) actual overall US prosperity (“Our Economy”), merely that of many of its corporations.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

US Corporate Profits- Patterns and Perspectives (11-1-11)

-1")