GLOBAL ECONOMICS AND POLITICS

Leo Haviland provides clients with original, provocative, cutting-edge fundamental supply/demand and technical research on major financial marketplaces and trends. He also offers independent consulting and risk management advice.

Haviland’s expertise is macro. He focuses on the intertwining of equity, debt, currency, and commodity arenas, including the political players, regulatory approaches, social factors, and rhetoric that affect them. In a changing and dynamic global economy, Haviland’s mission remains constant – to give timely, value-added marketplace insights and foresights.

Leo Haviland has three decades of experience in the Wall Street trading environment. He has worked for Goldman Sachs, Sempra Energy Trading, and other institutions. In his research and sales career in stock, interest rate, foreign exchange, and commodity battlefields, he has dealt with numerous and diverse financial institutions and individuals. Haviland is a graduate of the University of Chicago (Phi Beta Kappa) and the Cornell Law School.

Subscribe to Leo Haviland’s BLOG to receive updates and new marketplace essays.

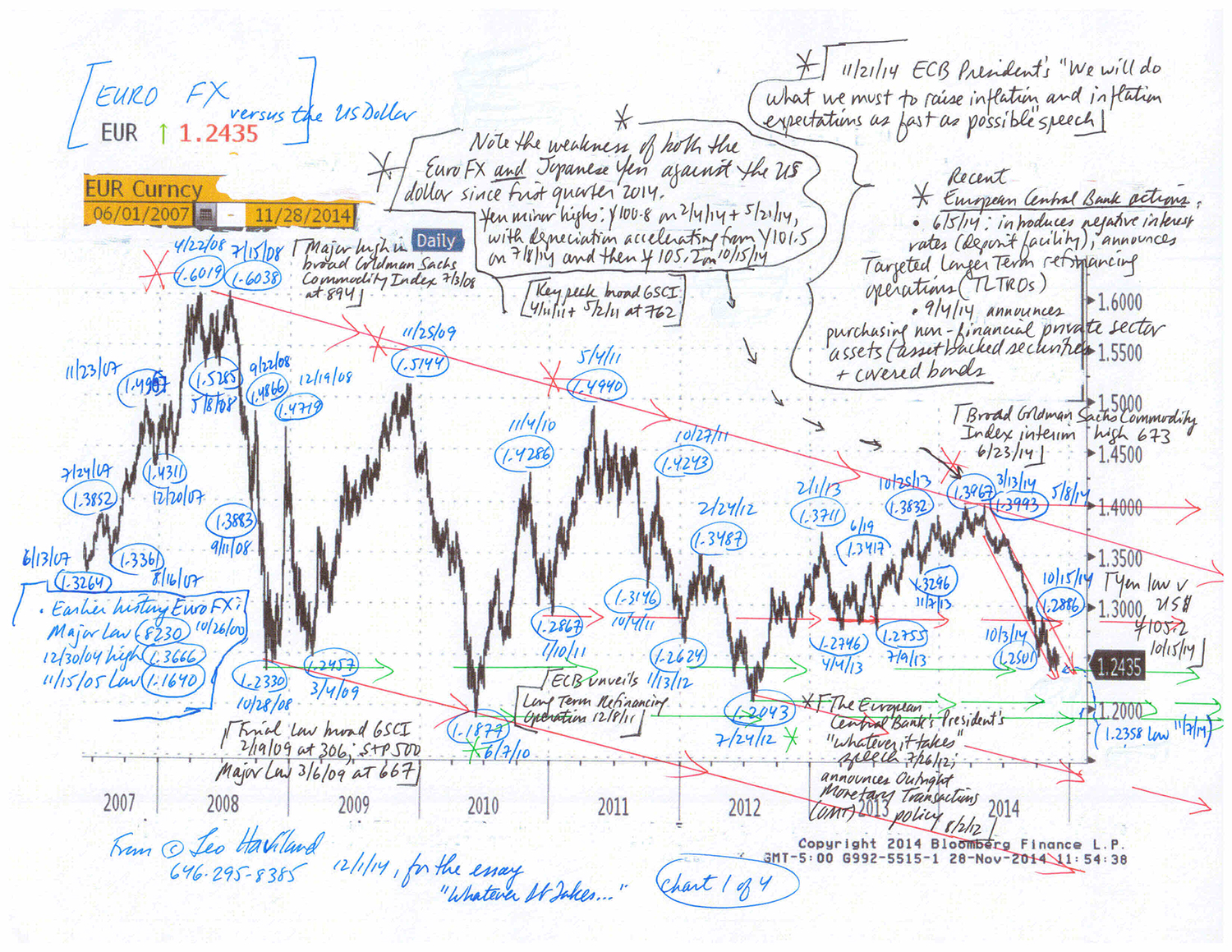

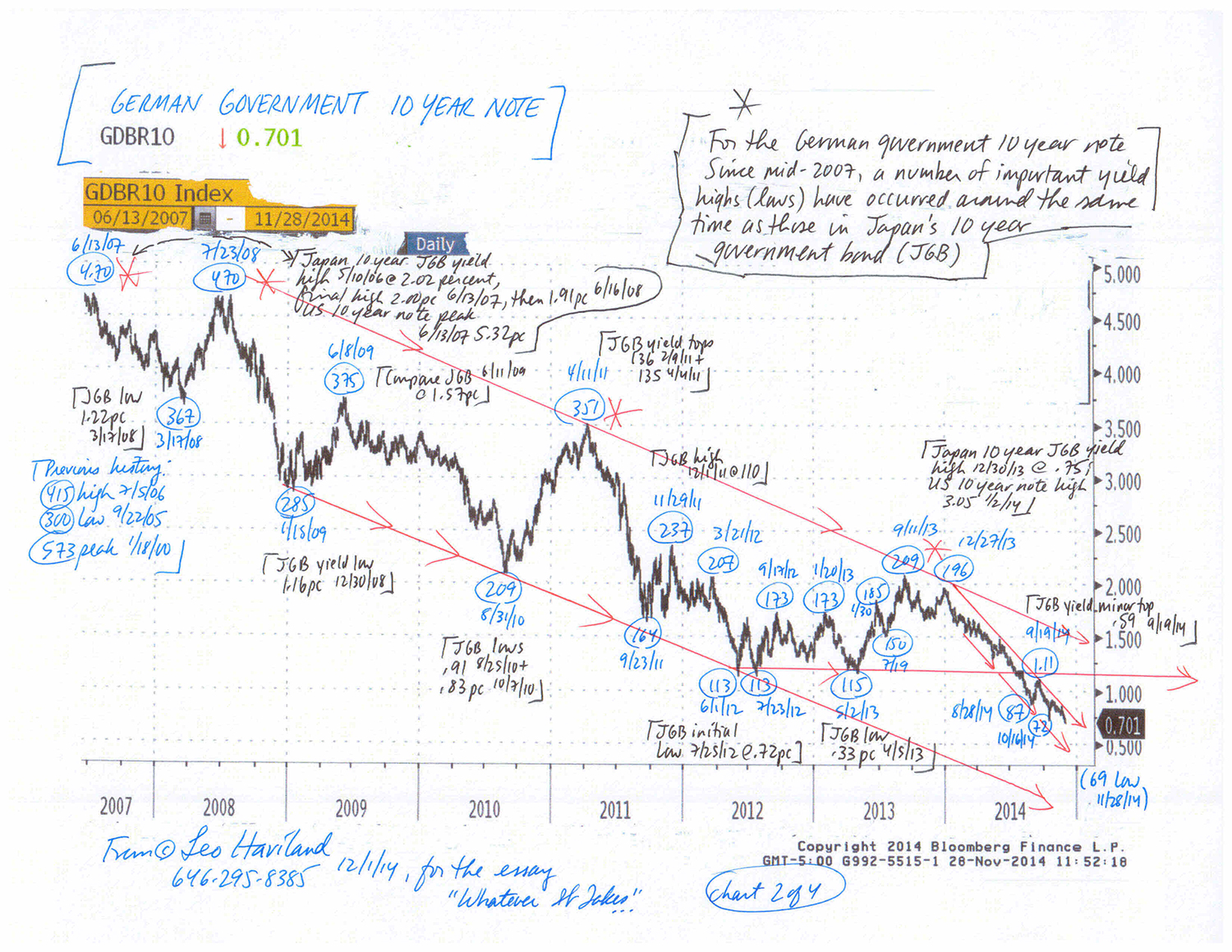

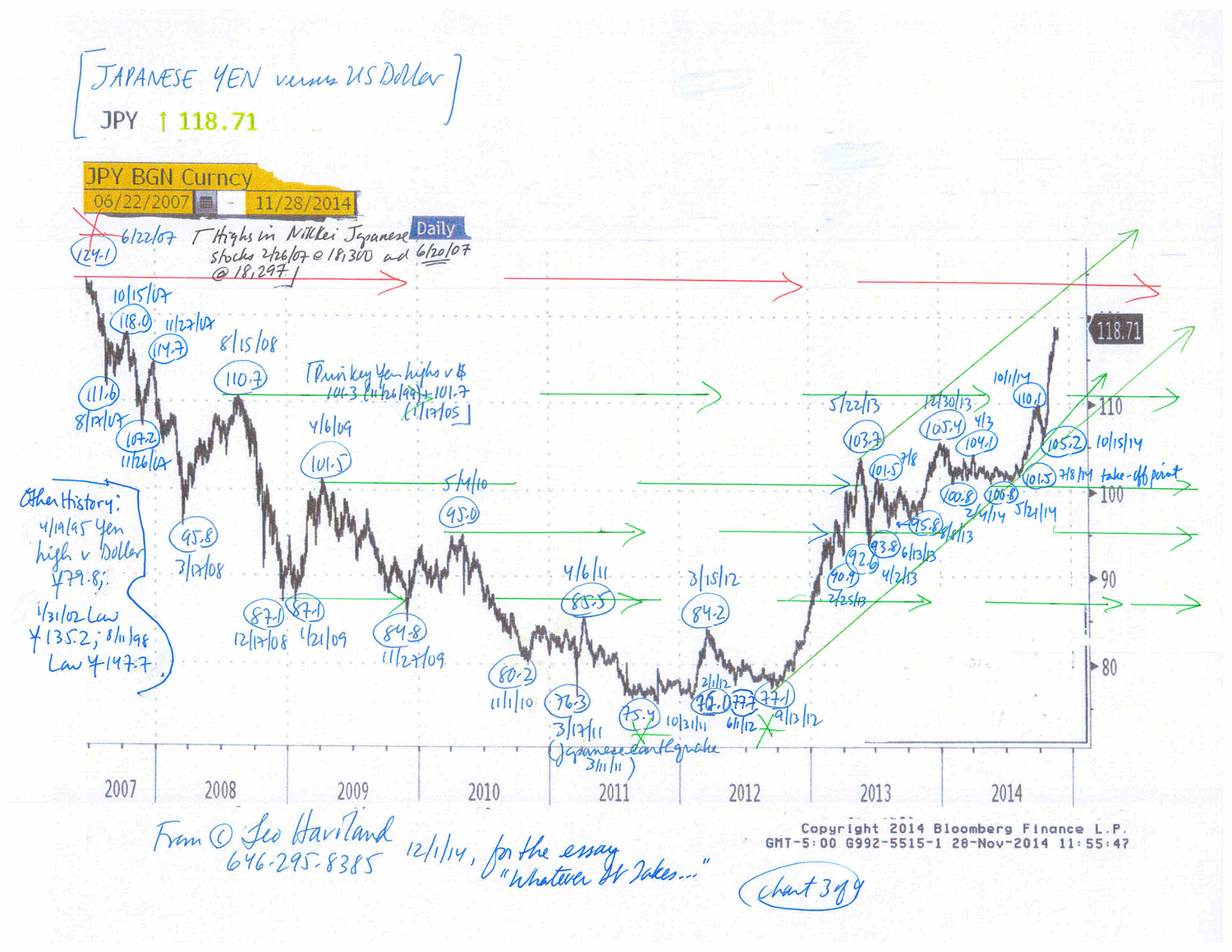

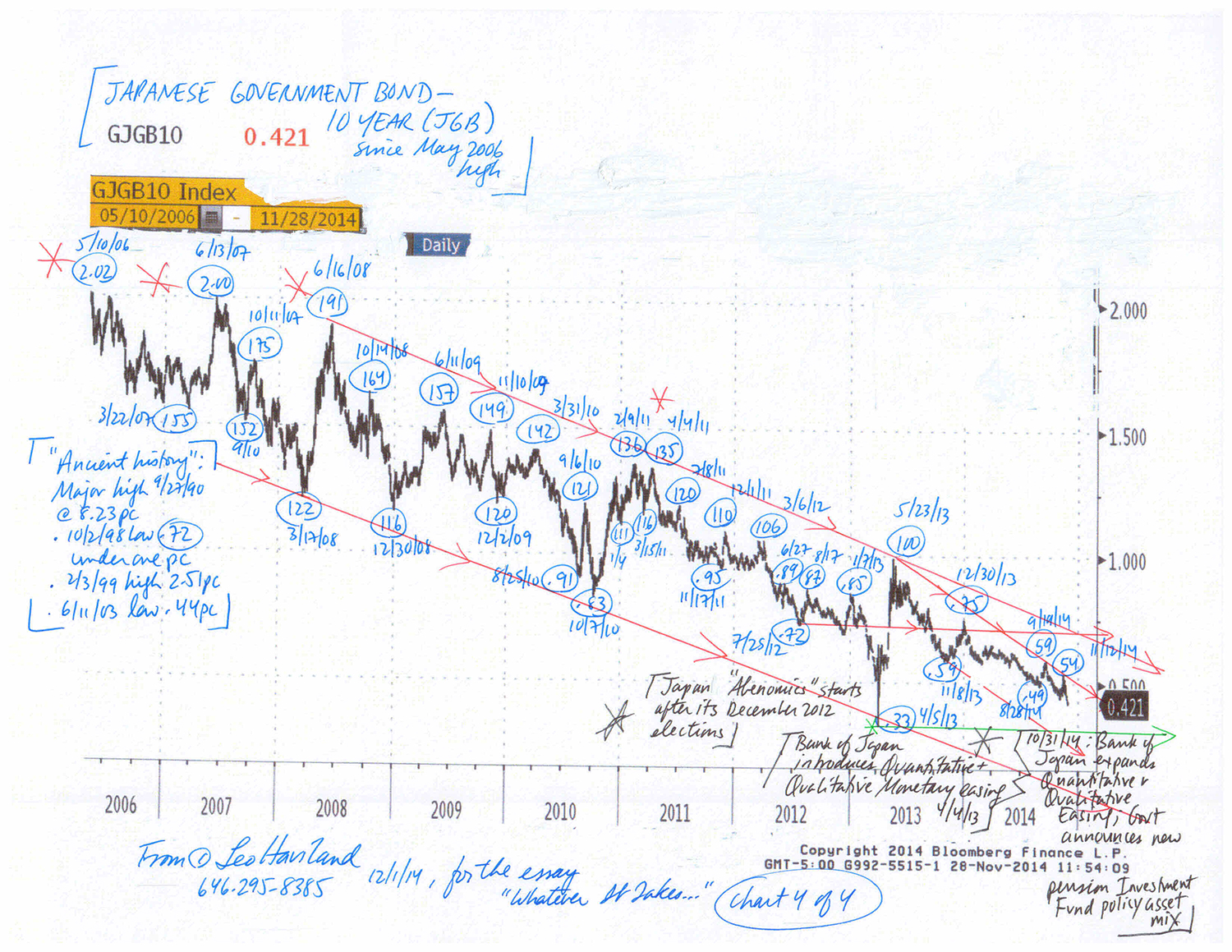

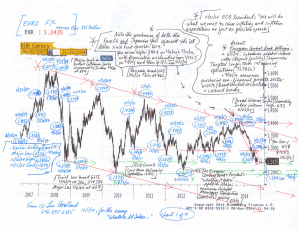

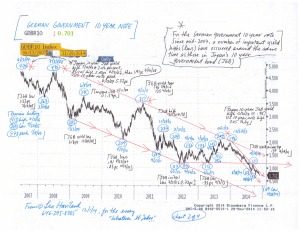

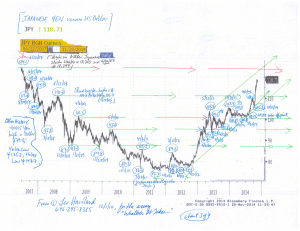

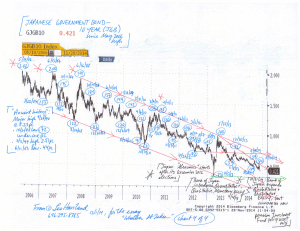

The Euro FX and Japanese Yen for several months have been weakening together, both against the US dollar and on an effective exchange rate basis. This currency relationship and bear trend will continue. Despite the Eurozone’s and Japan’s brave quests to create sufficient inflation (escape deflation), their success probably will be limited; inflation and longer term government interest rates probably will not sustain significant increases. However, even if substantial currency depreciation and massive money printing manage to achieve an inflation goal (and higher interest rates), they likely will not generate sustained economic growth.

Given that both the Eurozone and Japan suffer from low growth and deflationary challenges and fears, is weakness in the Euro FX connected with (encouraging that of) the Japanese Yen? Is the Yen’s swoon helping to depreciate the Euro FX? Are Japan and the Eurozone (and other nations) engaged in competitive devaluations (currency wars) to bolster growth?

One sign of the obstacles facing the Eurozone and Japan in their quest to boost inflation (and generate higher interest rates) is the recent behavior of the UST 10 year government note. American GDP recently has been robust, rising at an annual rate of 4.6 percent in 2Q14 and 3.9pc in 3Q14. However, the UST 10 year yield around 2.20pc remains well beneath its 1/2/14 top at 3.05pc. Admittedly the UST yield bounced up from the 1.86pc low of 10/15/14. But even since that mid-October 2014 depth, yields traveled up to only around 2.40pc, never piercing the important resistance around that level. The failure of UST yields to rally may signal future mediocre US (and worldwide) economic growth since yields generally advance during recovery (or hope of one).

Take the broad Goldman Sachs Commodity Index (GSCI) as a benchmark for commodities “in general”. It collapsed, of course aided by price dives in the petroleum complex, from 6/23/14’s interim high around 673 to under 520 recently. If sustained, this bloody price retreat will cut many statistical measures of inflation (and perhaps reduce inflation expectations). Thus it may encourage European and Japanese (and other) policy makers to embark on especially accommodative monetary policies. For example, the ECB may decide it has more need (justification) to quickly engage in massive QE, perhaps even by sovereign debt buying.

However, this GSCI weakness also may indicate underlying and ongoing risks to global economic growth as well as the difficulty of generating sufficient inflation in general. Moreover, sustained declines in petroleum prices may create crises in some producing nations that in turn spill over into other nations. For example, think of Russia (the ruble has moved over 50 versus the dollar), Nigeria, and Venezuela.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Whatever It Takes- Recent Eurozone and Japanese Adventures (12-1-14)

Charts- FX and 10 Yr Govt Note of Eurozone and Japan (12-1-14, for essay Whatever It Takes)

Many academic, financial, and political circles have long been married to “free market” ideologies. Nevertheless, the manipulation, maneuvering, or managing of a nation’s currency level and trends often occupies the deliberations and behavior of that territory’s central bankers, finance ministers, and many politicians. As in their efforts to control or at least influence interest rates (or stock marketplace trends), sometimes their reasoning, actions, and targets are explicit, often they are implicit.

Currency considerations are not islands apart from interest rate, stock, real estate, commodity and other marketplaces. So policy makers enamored of free market propaganda do not necessarily restrict their efforts to affect economic results to their home currency (or that currency’s cross rate relationship to one or more key trading partners). For example, picture the Federal Reserve Board’s longstanding yield repression policy, which has pinned the Federal Funds rate close to the ground.

Although the majority of currency observers and strategists focus their attention on crucial cross rates such as the US dollar against the Euro FX, broad real trade-weighted (effective) exchange rates influence important national policymakers. Analysis of these trade-weighted measures can unveil signs as to important (even if implicit) levels watched by central bank, finance ministry, and political guardians. Such trade-weighted foreign exchange measures consequently provide instruction as to potential strategy responses or changes by these often-vigilant sentinels. National and international policymakers of course are not the only ones looking and waiting around in marketplace games; Wall Street and Main Street likewise wait, watch, and act. Because these broad foreign exchange indicators (and the underlying cross rates) interrelate with perspectives on and decisions relating to current and potential elevations of and movements in numerous interest rate, stock, and other marketplaces, they offer insight into past, present, and future levels and trends of these arenas.

Dollar weakness does not necessarily (inevitably; forever) encourage or reflect a strong American economy or continue to help propelling US equities upward. Suppose a significant run against the “dollar in general” (TWD) occurs, whether via Chinese renminbi, Japanese Yen, or Euro FX (or other currency) strength against the dollar. A TWD dollar dive (especially under the July 2011 low) could force the Fed to significantly reduce or even abandon its interest rate repression and quantitative easing (money printing) policies. Consequently the effort by many American leaders and businesses promoting further weakness in the dollar relative to the renminbi may have some enthralling consequences not only for the dollar in general, but also for American (and other international) interest rate and equity marketplaces.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Currencies- the Waiting Game (11-4-13)

The broad real trade-weighted United States dollar will depreciate. Over the next several months, its retreat probably will reach July 2011’s record low around 80.6 (for the nearly four decades going back to 1973, monthly averages; March 1973=100) and break beneath it, with around 77.0 a reasonable target. Over the longer term, a descent to around 72.5 to 75.0 would not be surprising.

We know that all else equal, debtors (and borrowers) want as low an interest rate as they can get.

The Fed’s interest rate policy is (and has been for several years) geared toward aiding debtors (borrowers) at the relative expense of creditors (savers). Since debtors deserve special Fed help, surely the unemployed do.

We know that all else equal, debtors in a home currency (imagine the beloved US dollar) tend to enjoy some modest home currency depreciation. This makes their debt obligations less burdensome to pay off. This perspective assumes that these debtors can keep borrowing fairly easily, and at interest rates that not too high (overly punitive).

However, all else equal, foreign creditors are not enamored of such currency degradation. Foreigners hold an enormous amount of US Treasury securities, nearly $5.3 trillion (as of June 2012,

What happened to the US dollar after the Fed’s prior two massive rounds of quantitative easing? The TWD depreciated.

Significantly, the Fed’s determination to keep interest rates pinned to the floor (and thus offering pitiful returns on government debt relative to inflation) for an extended time period, say out to mid-2015, boosts the odds that its QE3 money flood will help to push the dollar down. In addition, recall that he TWD has been in a declining pattern over the past decade (or longer). So has America’s relative international economic and political prominence. Remember that QE3 is occurring alongside substantial US indebtedness (with a potential federal deficit disaster lurking on the horizon), a noteworthy current account deficit, and only modest domestic savings (compare Japan).

The Fed presumably is aware that the TWD declined after the QE1 and QE2 episodes. So apparently the Fed will tolerate dollar weakness to achieve its employment objectives.

FOLLOW THE LINK BELOW to download this market essay as a PDF file.

Fed Fixes and Dollar Depreciation (9-17-12)