GLOBAL ECONOMICS AND POLITICS

Leo Haviland provides clients with original, provocative, cutting-edge fundamental supply/demand and technical research on major financial marketplaces and trends. He also offers independent consulting and risk management advice.

Haviland’s expertise is macro. He focuses on the intertwining of equity, debt, currency, and commodity arenas, including the political players, regulatory approaches, social factors, and rhetoric that affect them. In a changing and dynamic global economy, Haviland’s mission remains constant – to give timely, value-added marketplace insights and foresights.

Leo Haviland has three decades of experience in the Wall Street trading environment. He has worked for Goldman Sachs, Sempra Energy Trading, and other institutions. In his research and sales career in stock, interest rate, foreign exchange, and commodity battlefields, he has dealt with numerous and diverse financial institutions and individuals. Haviland is a graduate of the University of Chicago (Phi Beta Kappa) and the Cornell Law School.

Subscribe to Leo Haviland’s BLOG to receive updates and new marketplace essays.

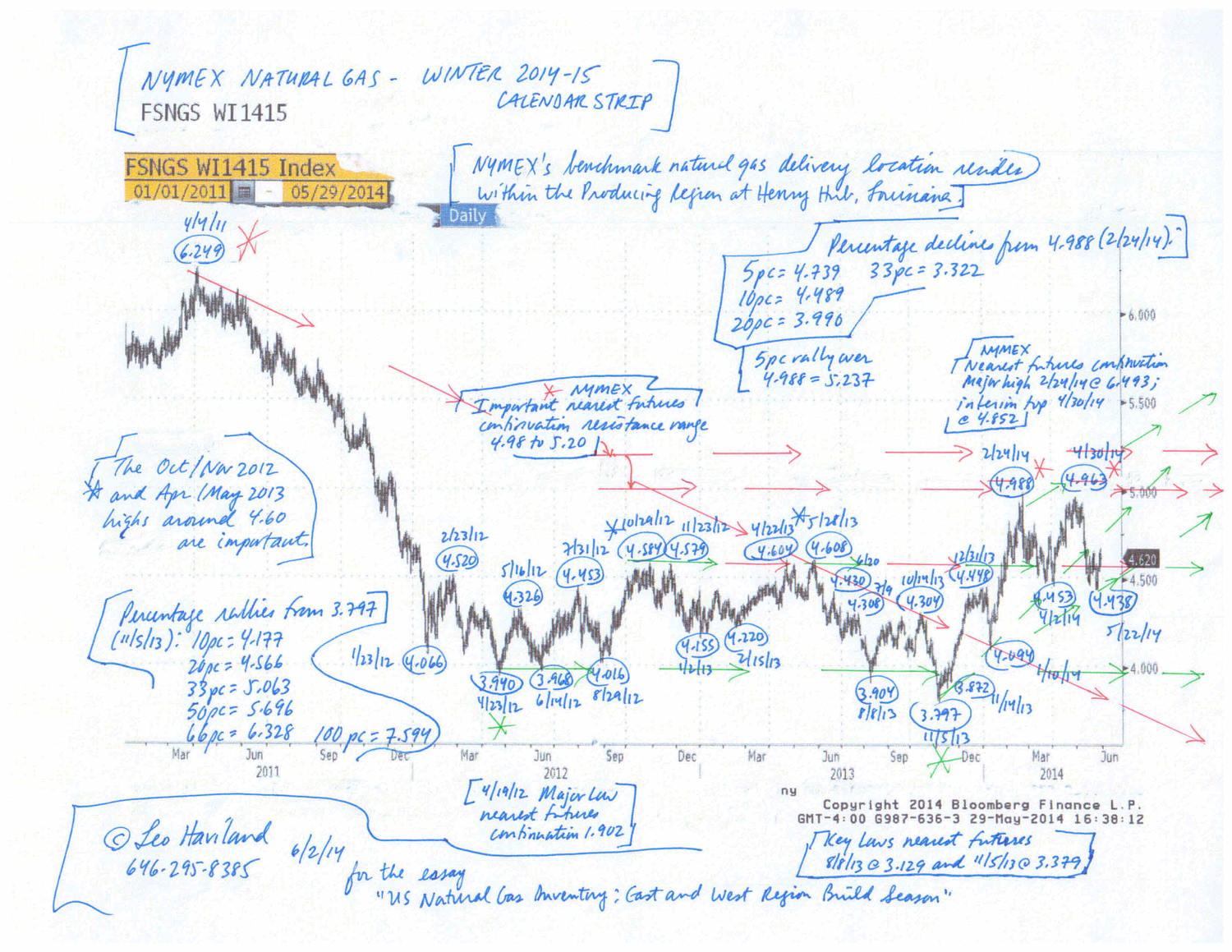

Assume normal weather and moderate United States economic growth. Then natural gas inventories in the US Eastern Consuming Region at the end of the 2014 build season probably will range between 1825bcf and 1930bcf. Around 2050bcf is about “normal” (average) for current United States supply and demand patterns. This current bullish inventory picture for the Eastern Consuming Region for the balance of build season parallels the bullish stock outlook of the US Producing Region.

Within the American natural gas scene, Producing Region and Eastern Consuming Region inventories have bigger marketplace shares than that of the Western Consuming Region. Is the Western Consuming Region’s inventory situation for build season 2014 bullish or bearish? The Energy Information forecasts that Western inventories will exceed 560bcf, a bearish perspective relative to that region’s 511bcf end build season average. However, the EIA probably overstates the likely amount of Western inventory building. Not only did Western stocks finish winter 2013-14 draw season at very low levels. Based on historical analysis of builds following comparable low starting totals, Western end build season inventories probably will be around 450bcf to 500bcf. This outcome is slightly bullish.

Despite the sharp price slump in NYMEX natural gas nearest futures continuation after its 2/24/14 peak at 6.493, the overall US inventory situation for the balance of 2014 build season remains bullish. The NYMEX natural gas complex during the course of build season probably will remain in a sideways trend. The NYMEX nearest futures contract probably will stay in a range from 3.80 /4.00 to 5.00/5.20. See “US Natural Gas Inventory Building: the Producing Region Picture” (5/18/14) for price forecast and Producing Region inventory details.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Natural Gas Inventory- East and West Region Build Season (6-2-14)

Chart- NYMEX natural gas winter 2014-15 strip (6-2-14, for essay US Natural Gas Inventory- East and West Region Build Season)

The S+P 500 high on 4/4/14 at 1897 probably is an important top. “US Stocks: Shadows and Signals” (2/3/14) remarked that “during the darkest days of the worldwide economic crisis of late 2008/early 2009 as well as during the subsequent recovery, Federal Reserve Board easy money policies have played key roles in encouraging bull moves in the S+P 500 (and many other equity playgrounds). Likewise, the elimination of some of these schemes, particularly previous rounds of quantitative easing (money printing), has occurred alongside highs in American stock benchmarks. What does tapering foreshadow? The Fed’s recent decision to reduce (taper) and eventually eliminate the current gigantic round of money printing warns that a notable top is or relatively soon will be in place.”

As it has in the past, the Federal Reserve will try to prevent a substantial stock marketplace tumble. But unless the S+P falls around ten percent, they probably will say or do little of note. However, if the S+P dives ten percent or more, the Fed lions probably will roar about their determination to sustain recovery. A slump of about 20 percent from a peak (especially if it occurs quickly) boosts the chances that they will slow their current tapering program.

Within and across fields such as stocks, interest rates, currencies, commodities, and real estate, the ardent hunt for sufficient “yield” by “investors” and others never ceases. Recall the glorious Goldilocks Era which preceded the worldwide economic disaster that emerged in mid-2007 and accelerated in 2008. As the Goldilocks Era neared its end prior to those dreadful days, packs of marketplace players eagerly foraged around in diverse (and sometimes very remote or complex) landscapes for adequate yield (good “investment” opportunities; fine returns). The global economic recovery began around mid 2009, with calendar year real GDP growth resuming in 2010. Over the most recent year or two in financial marketplaces (and especially currently), as during the late stages of the Goldilocks Era, the search for yield increasingly has become widespread and rabid. Such sustained heated quests, when reviewed alongside other indicators, warn of economic dangers.

FOLLOW THE LINK BELOW to download this article as a PDF file.

Money Jungle (4-14-14)

Charts- S+P 500 and others (4-14-14, for essay Money Jungle)